He Trusted His Employer’s Insurance—Then a Legal Letter Nearly Took His Home

Introduction: The Letter That Didn’t Feel Real

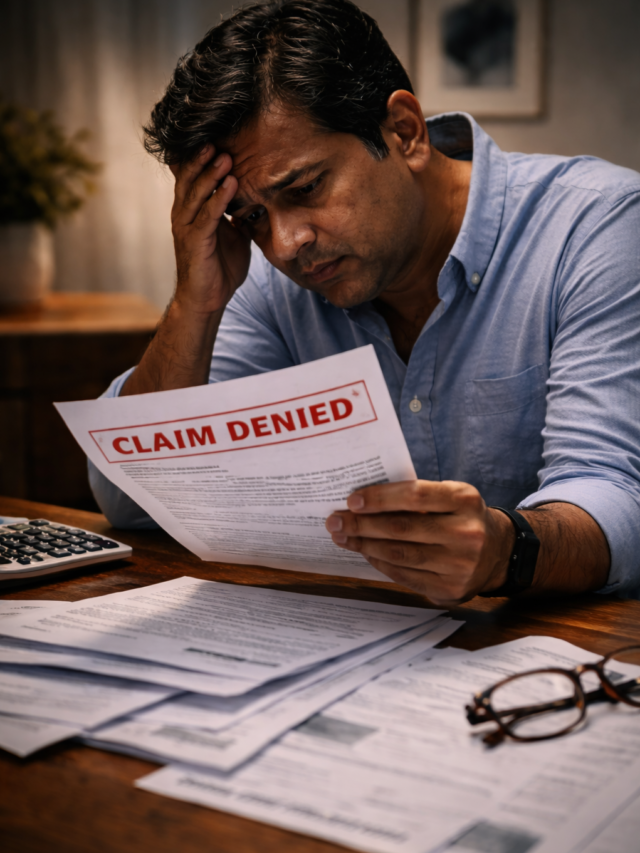

The envelope looked ordinary.

White paper. Black ink. No logo loud enough to raise an alarm.

David Miller almost ignored it.

It arrived on a quiet Friday morning, mixed in with grocery coupons, a bank statement, and a local election flyer—the kind of mail people usually open later.

But something about the envelope’s weight made him pause.

He slit it open casually—then froze.

The first line was bold. Clinical. Cold.

FINAL DEMAND NOTICE – OUTSTANDING MEDICAL LIABILITY

David read it once.

Then again.

Then he sat down.

Because nothing about it made sense.

He wasn’t uninsured.

He hadn’t skipped payments.

He hadn’t lied.

He hadn’t gamed the system.

For fifteen years, his health insurance premiums had been deducted directly from his paycheck—quietly, reliably, invisibly.

He had trusted his employer’s health insurance.

That trust was about to cost him everything.

A similar insurance mistake once changed someone’s life overnight.

A Life That Looked “Perfectly Safe” on Paper

David Miller was forty-six years old.

On paper, his life looked stable—almost boring.

He worked as a senior project manager at a mid-sized technology firm in the Midwest. He wasn’t flashy. He wasn’t reckless. He wasn’t the type to take unnecessary risks.

He had:

- A steady six-figure income

- A mortgage he paid on time

- Two teenage children preparing for college

- A credit score that hovered safely above 760

And most importantly—

Employer-sponsored health insurance.

The kind HR departments proudly advertise during orientation.

The kind of people they assume are “top-tier” simply because they come with a company logo attached.

David never questioned it.

Why would he?

Why Employer Insurance Creates False Confidence

Employer insurance feels safer than individual insurance for one reason:

Authority by association.

When a company provides insurance:

- Employees assume legal vetting

- They assume negotiated benefits

- They assume protections are automatic

HR presentations simplify everything:

- Colorful slides

- Bullet points

- Friendly phrases like “comprehensive coverage” and “peace of mind”

What they don’t show:

- The exclusions

- The termination clauses

- The continuation conditions

- The retroactive review rights

David never downloaded the full policy document.

It was 147 pages long.

Like most people, he assumed:

“If something mattered, HR would tell us.”

That assumption would later feel painfully naive.

Many people assume their career decisions are always safe—until reality proves otherwise.

The Symptoms That Didn’t Feel Dangerous

The first signs were subtle.

Fatigue that didn’t go away.

A dull ache that came and went.

A strange weight loss that felt almost welcome at first.

David blamed stress.

Deadlines. Meetings. Late nights.

When the pain became persistent, his wife insisted he see a doctor.

A few tests turned into more tests.

Then came the scan.

A Diagnosis That Changes the Meaning of Insurance

The oncologist didn’t waste time.

Stage 2 colon cancer.

The word “cancer” rearranges reality instantly.

But the doctor was calm. Confident.

“We caught it early. Treatment outlook is good.”

David’s fear softened into relief.

His very next thought wasn’t about survival.

It was about logistics.

“I have insurance. We’ll be okay.”

That sentence felt like armor.

When Everything Appeared to Work Perfectly

Over the next six months:

- Surgery approvals came through

- Hospital stays were authorized

- Chemotherapy sessions were cleared

- Claims were processed without friction

Each Explanation of Benefits email looked reassuring.

Approved. Paid. Processed.

The bills were massive—over $310,000 in total—but David never saw them as his problem.

Insurance was doing what it was supposed to do.

Or so it seemed.

The Silent Trap of “Conditional Approval”

What David didn’t know was that many employer insurance claims are approved conditionally.

That means:

- Approval assumes continued eligibility

- Eligibility assumes active employment

- Employment status affects coverage continuity

None of this is explained during treatment.

Because legally, it doesn’t have to be.

The Layoff That Changed Everything Overnight

Nine months later, the company restructured.

David’s department was dissolved.

The meeting was short. Polite. Corporate.

HR handed him a folder.

Inside:

- Severance details

- COBRA continuation paperwork

- A neutral smile

The COBRA premium made his stomach tighten.

$1,870 per month.

David hesitated.

Treatment was over.

Doctors were optimistic.

Savings were already strained.

So he declined COBRA.

That single decision quietly activated a clause he had never read.

The Clause That Almost No One Understands

Buried deep in employer health plans is something called post-termination claim reassessment.

In plain language:

- Insurers reserve the right to re-evaluate claims

- Especially long-term treatments

- Especially when employment ends during a care cycle

This isn’t rare.

It’s just invisible.

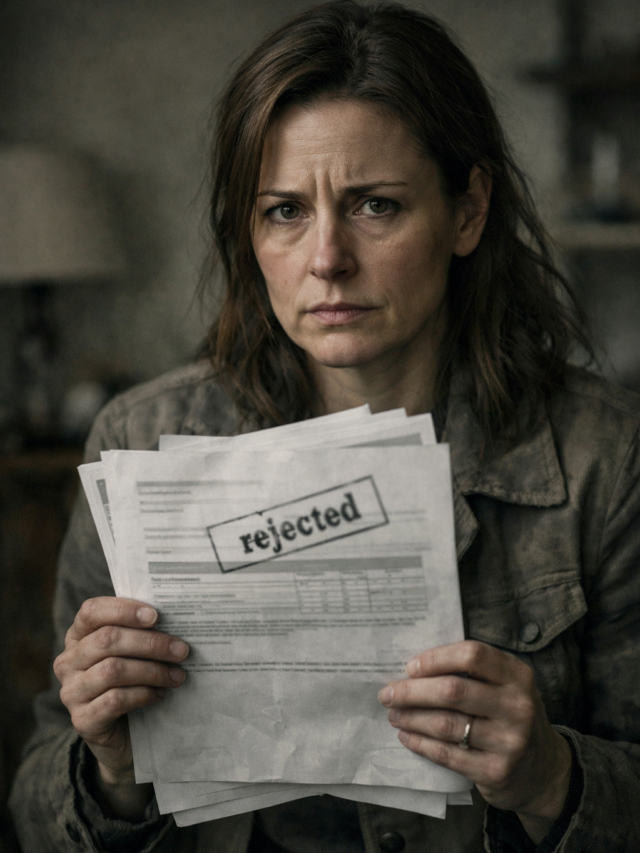

The Letter That Rewrote His Reality

Three months after the layoff, the letter arrived.

The insurer had reclassified part of his cancer treatment as ineligible.

Reason given:

“Loss of group eligibility during extended treatment cycle.”

Amount demanded:

$168,417

Payment window:

30 days

Legal escalation was threatened.

David thought it had to be a mistake.

It wasn’t.

Sometimes, a single unnoticed decision quietly reshapes insurance, career, and an entire life.

Why This Is Completely Legal

Employer insurance protects:

- The employer

- The insurer

Not the individual.

The policy terms were clear.

David had simply never read them.

Insurance law doesn’t care about fairness.

It cares about contracts.

The Financial Freefall Nobody Warns You About

What followed was slow, humiliating, and exhausting.

- Retirement funds withdrawn early

- Credit cards maxed out

- Loan applications denied

- The credit score dropped over 140 points

The cruelest part?

The hospital had already been paid.

The insurer wanted reimbursement from David.

Why Hospitals Stay Silent

Hospitals:

- Verify coverage at the time of service

- Do not track employment continuity

- Are paid upfront by insurers

Disputes later become the patient’s problem.

No one warns you because:

No one is legally required to.

Standing on the Edge of a Lawsuit

David consulted an attorney.

The advice was brutally honest.

“You can fight this.

But legal fees alone could cost $80,000.”

Negotiations dragged on for months.

The final settlement:

$96,000

Paid through a combination of loans and retirement savings.

David kept his home.

Barely.

What This Story Really Means for You

This isn’t a rare loophole.

It’s a structural feature.

Situations most at risk:

- Cancer treatments

- Pregnancy complications

- Mental health programs

- Rehab and long-term therapy

- Post-surgery follow-ups

Employer insurance is temporary protection.

Personal insurance is permanent control.

Warning Signs You’re Exposed Right Now

Ask yourself:

- Do you rely entirely on employer insurance?

- Do you know what happens after termination?

- Have you read the continuation clauses?

- Do you assume approvals are final?

If yes—

You’re vulnerable.

How David Lives Differently Today

Now he carries:

- An individual health policy

- Critical illness coverage

- A legal emergency fund

- Annual policy audits

His premiums are higher.

His stress is lower.

Moral of the Story

Insurance that depends on your job

depends on someone else’s decisions.

Before your next HR email makes you feel “covered”—

Read the policy.

Understand termination clauses.

Protect yourself beyond employment.Because the most expensive lesson

is learned after approval.